-

-

Marc Deschenaux

juriste financier, associé

Maîtrise en Droit Économique Certifié en Droit Transnational Baccalauréat en Droit

-

Hornblower.jpg)

Ralph (Ray) Hornblower

juriste, associé

Gérant du Bureau de New York Juris Doctor Avocat au Barreau de Washington D.C.

-

Guy Girod

Consultant Financier et Immobilier

FRICS (Membre de l'Institution Royale d'Experts Immobiliers)

Membre du Comité d'une Association

d'Autorégulation

-

Michael G. Horner

ingénieur & consultant, associé

Diplôme d'Ingénieur Diplômé en Sciences du Comportement

-

Sylvain Théodoloz

consultant en affaires

-

Bruno Chambardon

Consultant en Communication

-

-

Notre Cabinet est Membre de:

LA SOCIÉTÉ SUISSE DES JURISTES

La Société Suisse de Droit International

L'ASSOCIATION de JURISTES d'AFFAIRES INTERNATIONAUX

L'Association Internationale de Droit Économique

Experts Mondiaux en Droit

ORDRE des EXPERTS INTERNATIONAUX

Organisation Internationale Des Experts

Association Internationale des Avocats du Divertissement

La Société Genevoise de Droit et de Législation

L'Association Suisse de Private Equity et de Finance d'Entreprise

Cour Internationale de Médiation et d’Arbitrage

Swiss Finance + Technology Association

-

Recrutement

-

Notre mode classique de recrutement passe par le stage.

En savoir davantage sur un stage chez nous.

-

-

-

-

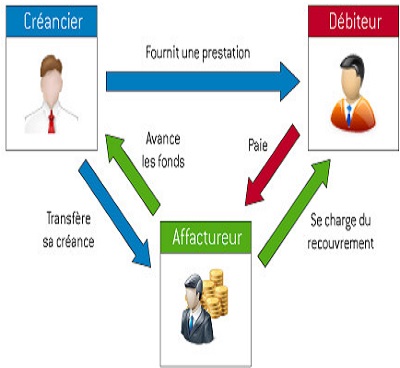

Affacturage

Généralement, les banques refusent de financer les sociétés qui en ont le plus besoin. En revanche, elles peuvent faire confiance aux clients de ces sociétés qui sont bien établis.

Découvrez comment financer votre société par l'Affacturage. -

Financement Privé

Lorsque les banques refusent de financer votre société ou votre projet, il vous faut accéder à un financement privé en capital risque.

Découvrez comment financer votre société par une émission privée, c'est-à-dire une émission de titres distribués de manière privée. -

Introduction en Bourse

Pour que les banques se bousculent pour financer votre activité, il faut que votre société soit transparente aux yeux de tous, donc publique.

Découvrez comment financer votre société par l'introduction en bourse tout en gagnant une fortune pour ses actionnaires.

-

-

-

Distribution

Découvrez comment développer une distribution internationale et puissante à bas prix.

-

-

-

Franchisage

Découvrez comment franchiser votre affaire sur le plan international pour un prix raisonnable.

-

-

-

Partners

-

Articles

Les articles suivants illustrent les travaux de recherche auxquels les membres de notre cabinet ont participé:

- Assomptions & Projections Financières

- Bid, Ask et Spread

- Blockchain

- Contrat de Travail & Modernité: Le Contrat de Participation en Industrie

- Contrat Intelligent

- Du Besoin d'Argent au Capital Privé Fonctionnement d'une Levée de Capital

- Elever une Licorne

- Finance, Economie et Monnaie - Définitions

- Financement Mezzanine

- La Compliance, un Prétexte d'Espion

- La Conceptualisation d'une Affaire

- La Dilution du Capital

- La Distribution Privée de Titres

- La Due Diligence

- La Factualité

- La Feuille de Termes (Term Sheet)

- La Notion d'Œuvre d'Art en droit de l'art

- Le Prospectus d'Emission de titres

- La Puissance de Un ou la Définition du Génie

- La Société Perpétuelle

- La Théorie des Objets en résumé

- La Théorie des Wagons appliquée aux IPOs (Initial Public Offerings)

- La Titrisation de Propriété Intellectuelle

- L'Accord

- L'Accord de Gentilshommes

- L'Accord de Principe

- Le Consentement Valable

- Le Contrat

- Le Contrat de Souscription de Titres

- Le Contrat d'Option

- Le Cycle de l'Action

- Le Financement (Financing)

- Le Jurist Non Avocat en droit suisse

- Le Montant Relatif - Partie 1: l'indice de Probabilité

- Le Pacte d'Actionnaires

- Le Plan d'Affaire ou Business Plan

- Le Private Equity

- Le Processus d'Egalisation ou " Matching Funds"

- Le Prospectus d'Emission de Titres

- Le Protocole d'Accord

- Le Réseau de Courtage de Titres

- Le Roadshow

- Le timing d'une levée de fonds ou Quand recevrons-nous l'argent?

- L'Echange d'Actions ou Swap

- Les Humeurs de l'Investisseur

- Les Pourparlers

- Les Titres de Propriété Intellectuelle

- Lettre d'Intention - 'LOI'

- L'idée

- Marché Primaire et Secondaire

- L'Introduction Publique Originale

- Marque Déposée: Quel symbole utiliser?

- Modèle d'Affaire: une simple définition financière

- Moment de la Naissance d'une Société en Droit Suisse

- Momentum

- Outil d'Ingénierie Juridique & Financière: La Boucle de Propriété

- Petite Histoire pour Comprendre les Droits d'Auteurs Musicaux

- Petite Histoire pour Comprendre les Droits Voisins Musicaux

- Pourquoi et Comment une I.P.O. (Introduction Publique Originale) génère de la valeur?

- Préhistorie Financière

- Principe d'Investissement et Levée de Capital

- Prix Progressif pour Accélérer la Distribution Privée d'Actions

- Reconnaître un Manipulateur ou une Manipulatrice

- Régulations d'Accès aux MarchésBoursiers Américains

- Secret, Confidentialité, Non-Divulgation

- Solidarité et Rupture de la Cote

- Sortie d'investissement ou Désinvestissement

- Trading International Imaginaire

- Une Méthode pour Franchir la Barrière d'une langue Etrangère

- Une Solution Simple à l'Inflation

- Une Vision d'Avenir pour l'Ordre des Experts Internationaux

- Voies d'Accès au Marché Boursier

- Votre société est-elle prête pour une Introduction Publique Originale (IPO)?

-

Dissertations

Les publications suivantes illustrent les travaux de recherche auxquels les membres de notre cabinet ont participé:

-

By reading the following text, you will understand the process of raising funds for your business. If you have any questions, they will be resolved by the end.

1.What reason should I use DHP and SIH

DHP offers a range of services such as private financing, bank credit, financial engineering, financial expertise, organization, restructuring and banking support.We also offer other legal advice on creation of legal entities, due diligence, corporate structures and establishment in Switzerland.Our goal is to help the entrepreneur realize their business dream and the firm does not participate in litigation.

2.How do I contact the firm

The easiest way for us to help you to make an appointment and come into our offices. You can do this at Swissjurists.com or call +41 22 510.25.00.

3.Can you help me with legal writing

This is a speciality. We can help with contracts, bylaws, resolutions, options and emption rights.

4.What other drafting can you help with

Financial drafting, commercial drafting, plans, short summaries and budgets

5.Can you tell me how to make a business plan

Of course. A business plan describes the new endeavour and explains its purpose and target market, It outlines market analysis, organizational and managerial structure, products and services and the marketing strategies for branding.

6.Do you have a shorter version

Yes, the executive summary, or short summary is a nutshell version.

7.Can I raise money based upon a business plan.

We would advise you to prepare a private offering memorandum. This is a legal document written by lawyers, which covers the main parts of a business plan. This is facts disclosed to investors through a lawyer.

8.So I use this to raise money

You can raise as much as your project requires, but this route is best suited when you need to raise at least USD 10 million.

9.Why should I not use banks and venture capitalists?

There are many alternative options, such as obtaining a loan from a bank or giving up equity to venture capitalists in return for finance.

10.In what country will I raise the money

We raise money through the United States market and specialise in this system.

11. Do I need to be a US based company and if so can you incorporate my company in the United States

Yes, this is the simple answer.

12. Why should I use the United States

Because of Liquidity and availability of capital in the US market. In simple terms this means you are much more likely to raise your money.

13. What is the mechanism by which the company becomes a US company

Through a stock SWAP

14. What are the main ways of raising financing

Through a Private Offering or an Initial Public Offering

15. Can I do a private offering and not an IPO

Yes, it is possible to raise money through just a private offering. A private offering is the process by which the company/ issuer issues securities for distribution in the private markets.

16. What are the questions that an investor usually asks

They will ask questions such as: how much do You need in total for Your project ? How do I recover my investment ?How long until I recovery investment ? What is my Guarantee? What are the risks ? Have You done it before ? What are the critical success factors ? What is in it for me ? How much profit can I make ?

17. When do we raise the money for a private offering

It depends. Investors may not invest. Large investment funds could invest in one day, but generally if they do this it is because they are protected by a strong due diligence process. The process typically takes six months to one year, but this can be affected by conditions.

18. Can anyone invest in a private offering

No, this is subject to legal regulation whereby the investor must be an accredited or, in other words, financially sophisticated or a financial professional.

19. How do I know if my company is ready for an IPO

You will be able to go public in the United States, with less stringent requirements for profitability than in Europe. The company should preferably be profitable or at least cash flow positive and have two years audited balance sheet.

20. Great and how do I make money from an IPO

The money that you make from an IPO arises from differences in valuation between the private and public market.

21. What do investors have to know about financing

The public market values the anticipation and to invest the investor needs to know that opportunity exists. In other words, he must be able to evaluate the gain/risk ratio.

22. Is there another way to go public apart from an IPO

Yes, either through a merger or reverse merger or through securities market forces.

23. Can you help me understanding the basic process of financing. What do I have to give up.

There are two main forms of financing. In the debt you will owe a sum of money to the investor which is the amount you have to obtain in addition to interest. With capital or equity, the investor will own shares in your company.

24. So with equity, will my shares be diluted by a new round.

Equity dilution involves stock or share dilution. This can result from : A primary market offering or an IPO, Employees exercising their stock options or Investors converting bonds into stocks.

25. Ok, so back to an IPO. What steps do I need to take to prepare for an IPO.

The process of an IPO takes shape over many months. Part of this is the due diligence procedure, which is the process of ensuring that the information contained in a file or prospectus is accurate and does not lend itself to a misrepresentation.

26. Can I pay for the IPO through a percentage of the money raised.

Commonly, DHP will require fees to be paid as the risk should be taken by the company and not the law firm.

27. What must I do for the due diligence

You must complete a due diligence plan, listing the purpose, objectives and issues. After this collect documents containing the alleged evidence and a history of due diligence. During an IPO each question and response must be entered into a due diligence history.

28. How does the roadshow work

The roadshow is a presentation organized by an issuer of securities and the syndicate of brokers and investment banks aiming at presenting to investors an opportunity of investment. The roadshow generates excitement and interest for the IPO.

29. Can I invest before an IPO and if so why would I

There are many reasons. This could be because there is a low price, there is a high yield, a very low break even point, low influence from the stock market, favourable IPO timing or a reliable audit.

30. When a person buys shares do they do so all in one go.

Not necessarily, the value may be different depending upon the timing of purchase. This is called the incremental price method.

31. Do investors require a legal document for the process

Of course. A subscription agreement is required for potential investors. This can be paid either directly to the Issuer or into a trustee account.

32. What is the incremental price method

This is the division of the securities into different phases. The price is calculated based on the risk associated with each phase. Thus there is more of an incentive reflected on a for early investment.

33. How long will the process take

The process of a Private Offering Memorandum will take 6 to 8 months, while an IPO can take two years.

34. Is there a quicker process

Yes, we also have a fast IPO service.

35. How are the securities distributed

A private offering is distributed through a private network connected to the firm DHP. A IPO takes place only through syndication.

36. What securities markets services can you help with

IPOs, bonds, and loans.

37.What are the questions that an investor usually asks

They will ask questions such as: how much do You need in total for Your project ? How do I recover my investment ?How long until I recovery investment ? What is my Guarantee? What are the risks ? Have You done it before ? What are the critical success factors ? What is in it for me ? How much profit can I make ?

38. What are the risks involved in this.

Disadvantages:The disadvantages are the non liquidity of investment, the access to liquidity, the risk of finality and the absence of a valuable history of background.

39. What are typical investment exit strategies

These include buyback of the shares of stock by the issuing company, acquisition of the shares of stock by a third-party, merger or reverse merger of the issuing company, exchange of the shares of common stock of the issuing company against those of a publicly listed company and Initial Public Offering (I.P.O.) of the shares of stock.

-

Bureau de Genève

Localisation: RUE François Bonivard, 10 1201 Genève - SuisseContactez-nous

Téléphone:+41 22 510.25.00

Fax:+41 22 510.25.01

Bureau de New York

Localisation: Madison Avenue, 340 10173 New York, New York -

Localisation

10100 Santa-Monica Boulevard - Suite 300

Los Angeles, California, 90067Phone:+1 310 594.20.48

E-mail: info@deschenaux.comContactez-nous

-

Politique de confidentialité.

Nous nous engageons à ne collecter aucun renseignement personnel, d'aucune sorte que ce soit.

-

MORE

MORE

more

MORE

MORE.

-

Philosophie

Nous sommes un Cabinet de juristes et non d'avocats car nous pensons qu'arriver au litige est déjà un échec. Nous ne croyons pas aux solutions émanant des tribunaux.

Notre équipe de juristes est entrepreunariale et tend à éviter les litiges autant que possible.

Nous croyons fermement que gagner de l'argent sur le malheur et les querelles d'autrui n'est pas un mode de vie harmonieux.

Cette attitude positive nous permet d'être crédibles envers nos clients pour des affaires importantes, parce qu'ils savent qu'ils engagent un représentant sans ennemis provenant de litiges passés sans liens avec eux.

Nous croyons que le juriste moderne doit s'allier à d'autres professions et compétences comme la finance, le marketing & la communication.

Notre profession est exactement à l'opposé de celle d'avocat.

Nous sommes des constructeurs gagnant notre vie sur les victoires, les succès et les réussites de nos clients et non sur leurs malheurs.

Généralement nous ne nous occupons pas de litiges.

Nous ne nous présentons devant les tribunaux que pour les sociétés que nous administrons ou pour les causes idéalistes gratuites.

-

Mission

Obtenir le Meilleur résultat possible

Nous sommes orientés efficacité

-

Vidéos

À propos de nous

What is Incorporation?What is an IPO?What is a Private Financing?What is Private Offering?

What is a Stock SWAP?

-

-

Global Law Experts

Ayant participé à 169 mises en bourse et à plus de 240 émissions privées, Marc Deschenaux a été reconnu par les deux organismes de la profession comme Expert Légal Mondial en Venture Capital.

Advisory Excellence 2018

Marc Deschenaux a également organisé plusieurs prêts gouvernementaux et la première annulation d'une dette nationale de l'histoire.

2016's Most Innovative Law Firm

Notre firme a reçu le prix de Firme la plus Innovante en 2016 pour l'invention de Marc Deschenaux: les titres de propriété intellectuelle.

-

MERGERS & ACQUISITIONS

Marc Deschenaux est le fondateur de Deschenaux Hornblower & Partners, LLP. Sa firme est une firme de juristes basée à Genève et à New York, spécialisée dans le financement des entreprises, toutes sortes de contrats commerciaux et financiers, la propriété intellectuelle incluant les licences, la franchise et la titrisation.

Ils disposent de sources de financement pour les entrepreneurs et les entreprises, afin qu’ils puissent réaliser leurs projets et leurs idées.

Ils sont experts mondiaux en droit du financement et d’organisation de financements pour les start-ups, les entreprises en croissance, ainsi que pour les institutions et les gouvernements.Venture Capital Law Firm of the Year in Switzerland

Le fondateur de Deschenaux, Hornblower & Partners, Marc René François Deschenaux, a commencé sa carrière professionnelle en tant que développeur de logiciel, créant des opportunités commerciales sur le marché des marchandises et des titres.

Il a conçu une partie du programme appelé « Autoarbitrage » qui avait pour fonction d’identifier les différents prix de titres et de marchandises, afin de déceler les opportunités d’arbitrage rentables.

A une époque où le commerce électronique était méconnu, le programme procurait un immense avantage en termes d’identification sur le marché.

Le programme était capable d'aider son utilisateur à identifier une opération rentable jusqu'à 105 minutes avant que les traders traditionnels n’y parviennent.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}